One of the main reasons for replacing the Group’s current core-banking platform with a digitally native platform like Thought Machine is to counteract the effects of open banking and the rise of fintech and Third Party Providers (TPPs). The rules require UK banks to share financial data on current account holders with challenger banks, fintechs, tech companies and credit reference agencies via secure application programming interfaces or APIs. These APIs can then be used, with the permission of customers, to open up the financial services industry to more competition and provide customers with products suited to their needs. So, with a swipe on a smart phone customers can find a better mortgage or compare household bills. At least that’s the theory. Members may recall that the use of APIs was one of the big ideas produced by the Competition and Market Authority (CMA) in 2014 for making the personal and business current account markets more competitive.

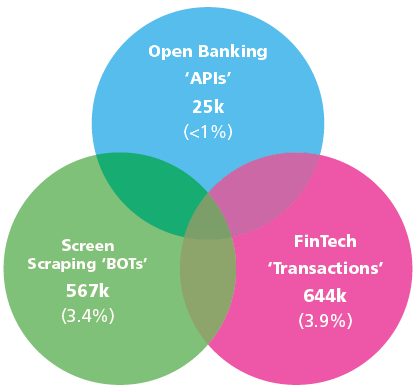

According to internal data seen by the union, 7% of active personal current account customers in LBG (see graphic below) use services including open banking APIs, Fintech transactions and screen scraping BOTs.

Although growth in this area is getting stronger by the day, it still only accounts for less than 1% of LBG’s active personal current account customers for each of the main Fintech providers. But it’s early days and according to research by PWC, a leading consultancy firm, more than 33m people are expected to sign up to open banking services by 2022. And don’t forget that in 1994 traditional booksellers didn’t think that selling books online would work. Amazon is now the largest publicly quoted company in the world. The first book it sold was on computers to a computer scientist using a T1 – connection. The rest is history.

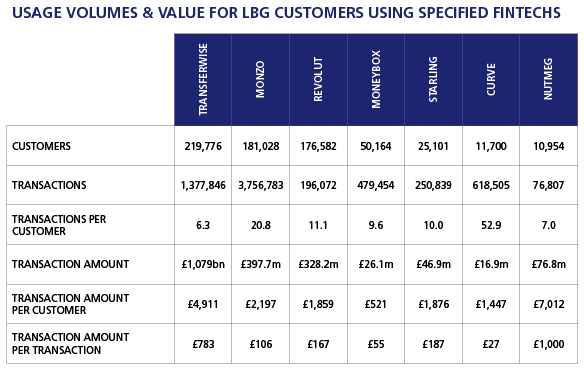

Monzo and Revolut have seen the biggest growth among LBG active personal current customers over the last two years. The table below shows the useage volumes and value of LBG customers using specific Fintechs over a 12 month period.

It’s true across all the banks but about 10% of customers produce 60% of the revenue that banks make from personal current accounts. If those customers with high balances and heavy overdraft usage are enticed away, the economics of retail banking will change forever. That’s why all the banks are scrambling to get out from under their legacy IT systems.

The TSB Factor.

The challenge for all the big retail banks, including LBG, is how do they move to digital platforms without causing IT meltdowns and customer chaos? Last week Lloyds, Halifax and Bank of Scotland customers became the latest to suffer a major IT crash when the ‘faster payments’ service suffered a major meltdown.

LBG will have looked at what happened at TSB with horror. That a bank’s IT system could collapse in the space of a weekend and a carefully crafted brand almost destroyed in a matter of weeks is a lesson in how not to do an IT migration. TSB’s IT meltdown has cost it £259 million so far but that’s likely to increase to £400 million, once you take in to account fines from the regulator.

Barclays, Natwest, RBS and Visa all suffered major IT outages last year.

The Treasury Select Committee has recently published a call for evidence on the common causes of computer and systems failures at financial services businesses. The Committee will look at the causes of disruption but also whether regulators are equipped to hold companies to account.

For more information on Thought Machine and The Vault please see this video from FinovateEurope 2018: https://www.youtube.com/watch?v=Q5ykML6Au6Y

We will return to Thought Machine again in future Newsletters, in the meantime, members with any questions can contact the Union’s Advice Team on 01234 262868.